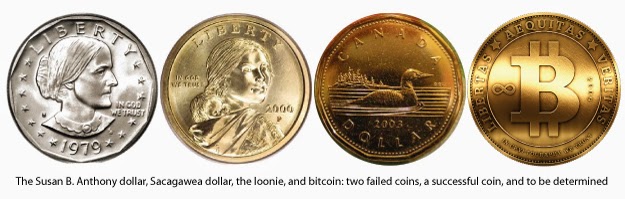

What causes a new currency to survive while others fail? Why do some cryptocoins never see the light of day while others enjoy successful launches? This post explores these questions by looking at the story of the Susan B. Anthony dollar, one of the great modern monetary failures.

Canada came out with a $1 coin in 1987 that remains in circulation to this day. We affectionately refer to it as the loonie as it carries a picture of a loon swimming on its reverse side. (The obverse side of a coin is the one that usually carries a portrait, the reverse side is opposite to the obverse side). The U.S. came out with a $1 coin in 1979, popularly known as the Susan B. Anthony dollar due to the appearance of the social reformer's face on the obverse side of the coin. Oddly, to this day the Susan B. Anthony is nowhere in sight. Americans don't hold it in their wallets or purses, nor do retailers keep them in their tills for change. Why did one monetary experiment fail and the other succeed?

The reason for introducing $1 coins is to replace relatively more expensive $1 bills. While notes are cheaper to produce than coins, the upkeep costs of a note issue are far higher than coin, especially as velocity increases. In general, higher value monetary instruments will circulate at slower velocities than lower value instruments. It makes more sense to use coins at the low-value/high velocity end of the circulation spectrum than bills because coins are both easier to sort and more durable—coins must be replaced every few decades whereas bills deteriorate within a year or two if they are used often. As the price level steadily inflates, what would have once been considered to be a high-value note that circulated only slowly enters the low value/high velocity end of the spectrum. Replacing that note with a durable metallic token makes sense... but that which makes sense isn't always that which succeeds.

One of the more popular reasons the has been put forward for the Susan B. Anthony's failure is that it was too similar to the already existing quarter in shape, size, and colour. This prevented consumers from quickly differentiating between the two coins. The loonie, on the other hand, was gold coloured due its bronze plating as well as having been minted with eleven edges to allow for differentiation when groping in one's pocket or purse. Apart from that, the weight and thickness of the loonie and Susan B. Anthony are almost identical.

I don't buy the argument that insufficient differentiation caused one coin to succeed and the other to fail. In 2000 the U.S. took another shot at debuting a dollar coin with the introduction of the so called "golden dollar" (due to yellowish tint provided by manganese brass), otherwise known as the Sacagawea dollar thanks to the appearance of this Native American interpreter and guide on its obverse. Despite having the same golden sheen as the loonie, the Sacagawea dollar does not circulate in the U.S. Rather, huge amounts of these coins are held along with their predecessor Susan B. Anthony in the vaults of the Federal Reserve as Fed officials wait in vain for demand to pick up. (See Lotz and Rocheteau for a good explanation of this event). That's two failed monetary experiments and counting.

|

| $1 coins languishing in a vault at the Federal Reserve Bank of Richmond's Baltimore branch Source: NPR |

Could it be that the loonie's eleven edges (the Sacagawea was smooth) were a sufficiently unique feature that the loonie stood out from the quarter and thereby successfully circulated? I don't buy it. That something so cosmetic as the shape of a coin's edge could push it into continued circulation seems silly to me. In all likelihood the Sacagawea dollar would have failed even if it replicated the loonie in every way.

The best explanation for the failure of $1 coins in the U.S. comes from Caskey and St. Laurent (pdf). They point to the network effects that must be overcome in introducing a new monetary instrument:

The benefit an individual attains from the use of a particular currency form depends on how many others are also using that currency form. For example, a new high-denomination coin can increase the range of vending machine transactions open to individuals, but only if vending machine owners convert the machines to accept the coin. Vending machine owners can increase sales from converting their machines to accept the coin, but only if the public commonly carries the coin. Similarly, retailers who learn to distinguish quickly the new coin can make small transaction more rapidly, but only if their customers have also learned to distinguish the coin quickly.In the presence of these network externalities, anyone who doubts that a new coin will be used by others won't bother spending the time and effort to familiarize themselves with the coin and make the necessary adjustments. If everyone behaves this way, the coin will never get off the ground. We get the unfortunate consequence that even though the substitution of notes by coin makes society better off, a set of perverse self-perpetuating beliefs prevents that solution from ever being selected.

So why did the loonie survive? Caskey and St. Laurent point out that the government stepped in to ensure that the network externalities that would surely have prevented the loonie's success were removed. In 1988, the year after the loonie's debut, the Bank of Canada announced that it would be withdrawing the $1 note from circulation. Consumers and retailers were given no choice but to adapt to the loonie's arrival. U.S. authorities, on the other hand, never tried to dash the existing network effects that favoured the status quo by withdrawing the $1 note. Because $1 bills and coins co-circulated, the public was given a choice between a perceived "good" currency, the existing and comfortable note, and a "bad" currency, an unfamiliar coin. They took the less costly route and stuck with the "good" notes.

Unfortunately this left the U.S. in the worst possible situation. Having failed to arrive at the welfare maximizing solution—the replacement of notes with coins—it was stuck not only with its existing and expensive $1 note circulation but it now had to pay ongoing costs for storing the unwanted coin.

This makes me think about the mad dash to create new cryptocurrencies. I remember a time when there were only five or six of them, but now there are around 313 cryptocoins according to Coin Market Cap. Many of the newer coins that have debuted over the last year are no doubt technically superior to Bitcoin, and the welfare of the universe of cryptocurrency users would surely be improved by the phasing out of bitcoin and the adoption of the best of these new coins. However, as the incumbent, bitcoin enjoys tremendous network effects. The public is already familiar with the various bitcoin wallets and client as well as the markets in which it trades and all the related bitcoin jargon that goes with it. Why bother spending the time and effort to understand a new cryptocoin if there is no guarantee that it will ever be widely accepted? Because everyone thinks this way, the cryptocurrency world has locked itself into an inferior currency structure. While it should be using something like SusanBAnthonyCoin, it still clings to bitcoin.

Or consider the current system. We could make the argument that the world would be better off it stopped using bank deposits, wire transfers, and cash and instead adopted bitcoin due to the latter's superior speed and low cost of maintenance. However, absent the cooperation of a large actor like the U.S. government to overcome the network effects that the existing system enjoys, it is unlikely that the technically superior option will ever be selected. Just like Susan B. Anthony dollars drift around as little more than a curiosity some 34 years after their debut, bitcoin may be no more than a neat curio in 2044 if the network effects that it faces are not overcome.

As for the $1 coin, at some point you can be sure that the U.S. will take its third swing at the bat. Let's hope that when the time comes they won't make the same mistake.

This Fed paper

ReplyDeletehttp://www.federalreserve.gov/paymentsystems/staff-working-paper-20131211.pdf

takes a negative view of the $1 coin. It even claims that the paper dollar is cheaper to produce.

An interesting experiment would be to reintroduce the paper dollar in Canada and see what happens. Would the new paper dollars be as unloved as U.S. coin dollars, or would they coexist, or would there be a big switch back to paper?

Max, thanks for the link --- so how are we supposed to reconcile the difference in opinions between the GAO and the Fed?

DeleteYep, that would be the definitive experiment in determining if network effects are as strong as Caskey and St. Laurent believe.

The GOA is mainly concerned with budget effects, so they emphasize the increased seignorage from $1 coins. But note that this is attributed to idle household inventories of coins, not greater usage of currency.

DeleteInteresting post, the durability aspect suggests that interest rates might be an important factor on what kind of currencies a government should issue. Perhaps now is the perfect time for reintroduction?

ReplyDeleteI believe they are currently releasing $1 presidential coins. http://www.usmint.gov/mint_programs/$1coin/

ReplyDelete"Could it be that the loonie's eleven edges (the Sacagawea was smooth) were a sufficiently unique feature that the loonie stood out from the quarter and thereby successfully circulated? I don't buy it. That something so cosmetic as the shape of a coin's edge could push it into continued circulation seems silly to me."

ReplyDeleteThis is a historical question. What kind of a way to answer it is this? "I don't buy it"? Are we now going to decide if Hitler invaded the USSR based on whether it "seems silly" he would have done so?

I don't buy it because it 1. doesn't jive with my intuition, and 2. a far better explanation exists in the fact that the Canadian government withdrew $1 notes so that the network effects enjoyed by the existing setup could not play a role.

DeleteWell, number 2 is a good reason.

DeleteJP, do you have any good knowledge about what the best cryptocurrency from a technical standpoint would be? What if the alternatives are just not good enough still. Are there any that have overcome the price stability problem? I just got this idea thats either pretty stupid or not but what if a cryptocurrency could by some algorithm not only make currency impossible to mine when the price of the currency is falling but suck up currency today by offering those who part with their currency more currency in the future. And on the other end when more currency is needed gives out currency to the people with currency options and/or make it easier to mine. All automatically adjusted to the level where price stability is achieved. Surely this beast of a crypto currency would overcome the network effects. :)

ReplyDeleteSome cryptocurrencies may have technical improvements over bitcoin -- e.g., blakecoin uses an algorithm that is more efficient to process, and has much faster and more reliable transaction times (talking by own book here). Most alt coin projects, however, are thinly veiled pump-and-dump schemes. The networks will dry up and the software will stagnate within a year. Regardless of the technical merits of various alt coin implementations, only people who are participating in the scheme (or making money by defeating the scheme) would rationally invest in an obvious pump-and-dump. Bitcoin's core developers are focused on improving the software as the basis of a payments network. They are not the most competent cryptography / software networking folks around. But Bitcoin's software is tested continually by thousands of hackers all over the world, with different skills and agendas. If the network can stand up to continual exploit attempts, it will continue to evolve and improve at a more rapid pace than parallel currencies that do not have as strong an ecosystem. I don't think it's a matter of adoption critical mass. Not even bitcoin has achieved critical mass as a payment system. At this stage it's more about setting up a feedback loop between real-world testing and effective integration of pull requests back into the core software.

ReplyDelete