|

| WWI Liberty bonds, which according to Neil Wallace circulated alongside Federal Reserve notes [source] |

What follows are some thoughts on the coexistence puzzle as well as the folks who find it interesting.

There is plenty of hyperbole over the difference between freshwater and saltwater economists, but one peculiarity that surely distinguishes a freshwater economist from his saltier cousin is that they tend to be interested in the underlying motivations guiding monetary exchange, the so-called microfoundations of money. (Saltwater economists tend to be content with broad assumptions about monetary phenomena). Representatives of the microfounded approach, which includes the blogosphere's own David Andolfatto as well as Stephen Williamson—who has anointed his approach New Monetarism—like to refer to their models as "deep models of money".

One of the classic questions that continues to interest deep money types is the so-called coexistence puzzle. Zero-yielding financial assets like central bank-issued banknotes are "dominated" in terms of rate of return by interest-yielding financial assets created by governments. The puzzle that needs explaining is why these dominated instruments can continue to coexist with the instruments that do the dominating.

A quick answer is that a lower-yielding asset can coexist with the higher-yielding asset because the first is more liquid than the second. In an uncertain world, the stream of liquidity services that an asset provides over its lifetime is a valuable service. An asset that provides a little less income can still be demanded in the marketplace as long as it provides a little more liquidity. Deep money folks would say that my answer is a bit shallow. It avoids exploring both the qualities of the assets being used and the frictions that characterize the world in which those assets trade that might render one asset more liquid than the next.

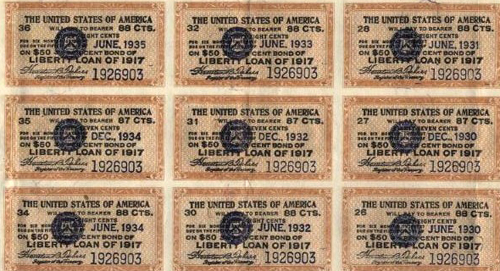

Let's explore the setup of the coexistence problem in more detail. In a 1982 paper, deep money pioneer Neil Wallace defined the problem thusly; if the government were to issue small denomination bearer bonds, say in units of $5, $10, and $20, and these instruments were to yield interest, just like their larger denomination relatives, why would anyone carry 0% Federal Reserve notes in their wallets when they might own an interest-yielding replica instead? These two instruments shouldn't coexist—cash should be driven out of existence or, if they are to coexist, then bearer bonds should yield no more than the 0% rate on cash.

One aspect of the problem, Wallace noted, was that for some obscure reason, governments typically choose not to issue small denomination bearer bonds. The large denomination size of t-bills and t-bonds inhibits their use in trade, thus preventing at the outset any sort of direct competition between government bonds and zero-yielding cash.

However, Wallace pointed out that this doesn't explain why private issuers don't simply buy high denomination government bonds and create their own government bond-backed small denomination bearer notes. If they did so, Wallace believed that two things might happen. These private issuers, by virtue of paying interest on their notes (more specifically by issuing bearer bonds at a discount to face value and allowing them to appreciate in price till maturity, much like treasury bills) would drive inferior 0% yielding banknotes out of existence so that only interest-bearing notes circulate.

Alternatively, the public would allow privately-issued bearer bonds to circulate at par with existing currency. Par acceptance would mean that private bearer bonds no longer paid interest in the form of a steadily rising price. However, Wallace stumbled upon an interesting side effect of par acceptance: nominal rates on government bonds would have to fall to zero. Why? According to Wallace, arbitrage dictates that as long as the rate on long term government bonds is above zero, competing private issuers will flock to buy those term bonds with which to back their 0% bearer notes, putting upward pressure on bond prices and downward pressure on yields. It makes sense for banks to do so because they earn the spread between the 0% notes that they issue and the interest-yielding bonds they purchase. According to Wallace, the arbitrage window will only be shut when banks have driven long term rates close enough to zero that the the opportunity for excess profits disappears. In a free market, the term structure of interest rates disappears. All we have is a flat yield curve.

Here is Wallace: "Thus, my prediction of the effects of imposing laissez-faire takes the form of an either/or statement; either nominal interest rates go to zero or existing government currency becomes worthless."

Of course in the world we live interest-yielding bearer currencies have not kicked out 0% notes nor have private notes driven long term bond rates to zero. Wallace attributed this to various legal restrictions against banks from entering the small denomination bearer bond line of business. Take away these legal restrictions and he believed that his conclusions followed.

Even if we removed these legal restrictions, I'm not convinced by Wallace's arguments. Given free competition in note markets, I don't think that positive-yielding small denomination bearer bonds (issued either by a private bank or a government) must necessarily drive cash into exile, not do I think their coexistence means that the term structure of interest rates must be flat.

To start with, the necessity of calculating interest payments throws a wrench in the smooth transfer of a bearer asset, a point made by Larry White. Say that the bearer bonds are printed with a $10 face value but sold by the government at a discount to face so that their price appreciates over time until maturity, the capital gain being a stand-in for interest payments. Should someone wish to use their unmatured bearer bond to pay for something, they will have to calculate how much of a discount to face to apply to the bond. Such a calculation imposes a burden on the transactors since it will take time to crunch the numbers or require a costly technology to speed up the process. As White has noted, a $20 note held for one week at 5% interest would yield less than 2 cents. Is it really worth it for a banknote user to take the time and trouble to compute and collect such a small amount?

The interest rate feature of bearer bonds also precludes the simple summations that round numbers allow. An owner of a $10, $5, and $20 bearer bond doesn't have $35 in purchasing power. Rather, discounting the bonds will show that their purchasing power is composed of inconvenient sums like $9.33, $4.89, and $19.60. This makes it harder to know how much purchasing power is in one's wallet prior to going to market, thereby inhibiting the usefulness of bearer bonds as a liquid medium. Carrying around 0% currency which trades at its face value allows for certainty of purchasing power, a feature that may more than compensate for lack of a pecuniary yield.

Even worse, having inconvenient non-round bonds in one's wallet or till makes the process of obtaining or providing change a nightmare. If you buy a $10 bottle of wine with an unmatured bearer bond worth $11.56, what are the odds that the cashier will have a $1.56 bearer bond to give you as change? 0% cash may not offer interest payments, but at least the standardized even denominations in which it is available (combined with small change) allow for hassle-free transactions.

Lastly, all transactions in bearer bonds face capital gains taxes. That means on each exchange, the owner of bearer bonds must fish back into their records to find the original price at which they received the bond, determine the price at which it was sold, compute the profit, and then submit all this information to the tax authority. Payments made with 0% banknotes are not taxed, saving those who choose to transact with banknotes time and energy.

So in a nutshell, the previous factors may explain why interest-yielding small denomination bearer bonds will always be less liquid relative to 0% yielding cash, thus preventing the former from kicking the latter out of circulation.

If Wallace's first point is wrong and the payment of interest on banknotes doesn't drive existing 0% cash out of existence, what about his second prediction? Assuming that privately issued bearer bonds are accepted at par, what prevents profit-hungry banks from issuing 0% bankotes and accumulating interest-bearing bonds, eventually arbitraging bond rates down to zero?

As I've already illustrated, interest yielding instruments (especially large and ungainly ones like t-bills) will always be less liquid than cash. This gives rise to an un-arbitrageable wedge between the yield on cash and that on bonds, or a liquidity premium. Note-issuing private banks eager to earn more spread income may be able to temporarily push rates down through bond purchases. However, at these lower bond rates the marginal bond investor will be dissatisfied. They are now holding an asset that offers the same inferior liquidity return as before but less interest. These investors will sell their bonds, in the process pushing interest rate right back up to so that bonds once gain offer an attractive return on the margin. In short, bond-buying banks can't push long term bond rates down to zero because the rest of the liquidity-buying public won't let them.

But if long term rates won't budge when banks buy them, doesn't that mean that banks can continuously earn excess profits by perpetually issuing 0% notes and purchasing risk-free long term bonds? Free dollar bills left on the floor are, after all, the biggest no-no in economics. This ignores the fact that even if rates don't fall to zero, other costs will rise instead as banks compete to enjoy the spread. Larry White refers to this as non-price competition. It might include any number of costly strategies used to attract note-holders, including longer bank operating hours, more tellers, increased advertising expenses to make notes more trusted, and special engraving of notes to make one's bills more attractive relative to the competitions'. Thse mounting costs will soon counterbalance the fat spread income, thereby reducing the window for excess profits.

So contra Wallace, laissez faire doesn't reduce the risk-free bond yield curve to a flat line. Because liquidity differentials between bonds and notes will continue to exist free market or not, bond rates will always have to provide a sufficiently high nominal interest rate in order to attract holders.

What makes Wallace's conclusion about the yield curve in a free market interesting is its pleasing counter-intuitiveness. Many of the theories that deep money people come up with have this same quality, including one of my favorites: the irrelevance of open market operations, or what some call Wallace Neutrality. Stephen Williamson's odd theory that central bank's need to fight inflation by lowering rates, not increasing them, is in this same tradition, although in this case I think he's probably wrong.

Empirical evidence is the best way to test deep money theories. In the case of Wallace's legal restrictions theory, reality is not kind. For instance, we know that in the 18th and 19th centuries Scottish banks were not burdened by legal restrictions on the issue of notes, yet the Scottish yield curve was not a flat one. Indeed, interest bearing bills-of-exchange circulated freely with notes. Despite dominating notes, bills of exchange did not drive them to oblivion. Makinen and Woodward report on the coexistence of small-denomination interest-paying "bons" in 1920s France with the franc currency, and Wallace himself points to evidence that Liberty bonds circulated concurrently with Fed cash during WWI. (I should note that David Andolfatto is skeptical of these instances since they are commonly associated with periods of fiscal distress.)

As for some of the more modern deep money efforts like Stephen Williamson's, reality remains a hard customer. One wonders how Rudolph Havenstein's tight interest policy would have created the Wiemar hyperinflation, for instance. While I'm being tough on the deep money folk, I want to sign off on a positive note. Figuring out the underlying nature of monetary exchange is no doubt an important endeavor. Anyone who wants to learn more about monetary phenomena and central banking should probably be reading what the deep money people have to say.

Another interesting post.

ReplyDeleteI'm trying to understand the mechanics of Wallace's second possibility. To make the private notes generally acceptable, issuing banks would need to undertake to convert them at par for deposit accounts and then potentially for transfer to accounts at other banks. It would then seem difficult for them to actually force an excess of notes onto the general public. If the public held more notes than they wanted, would they not just deposit them back with banks again? So the demand for bonds to back the notes would be limited by the amount of notes that people actually want to hold.

Nick:

DeleteExactly right. A good analogy is the minting of 1 oz. silver coins. A mint might try to "force" 10x more coins into circulation, but of course the excess coins would be melted back to bullion. Or suppose that a customer brings 1 oz to the mint, and the mint, rather than stamping it into a coin, puts the silver in its vault and hands the customer a 1 oz paper note instead. Here again, there can be no "forcing" of notes into circulation.

Or take it one step further and suppose that the mint starts issuing those 1 oz notes to anyone who brings in 1 oz worth of bonds, land, or anything else. Once again, "forcing" wouldn't work, but the law of reflux works just fine.

Nick, as best I can tell Wallace does not bring deposits into the picture and assumes only bearer notes and bonds, at least in the paper that I linked to. But I do agree that convertibility makes it impossible to force notes upon the public and would therefore limit the demand for bonds to back them.

DeleteBut deposits introduce another coexistence puzzle... why do 0% notes and interest-yielding deposits cohabit given that the latter dominates the other?

I've sometimes wondered why some respected bank hasn't tried to compete head-on with the Fed in "dollarized" countries. The Fed provides poor service outside the U.S. A private company could make its 0% notes attractive by keeping them crisper and cleaner and supplying the desired denominations. Well, maybe the market is just too small.

ReplyDeleteMax:

DeleteI think it's because the high cost of printing and handling paper money makes it unprofitable for most issuers. Nineteenth century note-issuing banks usually said that note issuance was unprofitable, and they only did it as a good form of advertising.

Also, banks outside the US have long been able to issue eurodollars in the form of checking account dollars. There is nothing to stop some of them from issuing paper eurodollars (on blue paper instead of green, let's suppose). The fact that none of them have done it indicates that the printing and handling costs would make it unprofitable.

Max, interesting point, but does the Fed actually provide poor service outside of the U.S.? I've traveled in Angola and don't recall ever seeing a worn out U.S. dollar note. Kwanza notes issued by the Angolan central bank were often filthy. If I recall correctly, the Fed maintains a network of foreign distribution centers... let me see, aha, here's a link:

Deletehttp://www.bis.org/publ/bppdf/bispap15r.pdf

Read sections 4 and 5 describing the Fed's extensive international note operations. The reason that private issuers may not have tried to issue competing dollar notes is they are competing against a very well-run monopolist.

Mike, I have a hard time with the idea that note issuance wasn't profitable. It seems odd to me that corporation would develop and maintain a money-losing business. The Canadian banking system in the 19th c. had open competition in note issuance yet were very staunch in trying to resist government attempt to force them to give up their ability to issue notes. When they lost the ability to make $1 and $2 notes, they started to issue $7s!. Why go to such an effort if they couldn't make a buck? (I see you made the same point on that post too.)

JP:

DeleteI meant "unprofitable" in the textbook sense of the zero-profit theorem, which is to say, the note issuer just earns a competitive rate of return, but doesn't get a free lunch.

I think printing and handling costs are the key to the coexistence puzzle. If a bond has no P&H costs then it will yield 5%. If another bond has 3% P&H costs, then it will yield 2%. Another bond might cost 5% and yield 0%, while another bond might cost 7% and yield -2%. Each of those bonds will have its niche of people who want to hold it in spite of its low return, because the bond yields some kind of convenience, like monetary liquidity. Once this is recognized, the puzzle of why some people hold 5% bonds while others hold -2% bonds just goes away.

I agree. A bank that endures higher printing and handling costs does so to promote the liquidity and conveyability of their securities which in turn should allow them to reduce the yield they must offer on those securities.

DeleteGreat post JP. Re:profitability of note issuance.

ReplyDeleteNote issuance now may not be profitable, vs. 100 years ago (with Molson money) because of modern accounting regulations. E.g. how harsh accounting treats gift card issuers, airline points plans etc.

Even for the government, I've always wondered how much 'true" seignorage the BoC/Mint earns on currency/coins. The government doesn't actually buy anything directly with those coins (only indrectly via open market ops). People just love to collect special edition coins (like stamps before), but I would say those are novelty profits, like the CBC selling T-shirts.

jt26, the Bank of Canada earned a cool $1.3 billion last year, which isn't too shabby. The Royal Canadian Mint earned $36 million. It helps that they're monopolies.

Deleteif the low denomination bearer bonds were on a phone app I dont think most of your objections would apply...

ReplyDeletealso the capital gains tax is just a slightly lighter form of legal restriction so by assumption shouldn't we ignore it in the analysis ?